Digital Dives

Over the past decade, private credit has emerged as one of the fastest-growing areas in global finance, driven by a shift in lending dynamics. Where banks once dominated commercial and institutional lending, today private investors—ranging from specialized funds to larger alternative asset managers—are stepping into roles traditionally held by financial institutions. This phenomenon, though widespread across multiple asset classes, holds unique potential in the cryptocurrency market, where access to credit remains constrained by regulatory and structural barriers.

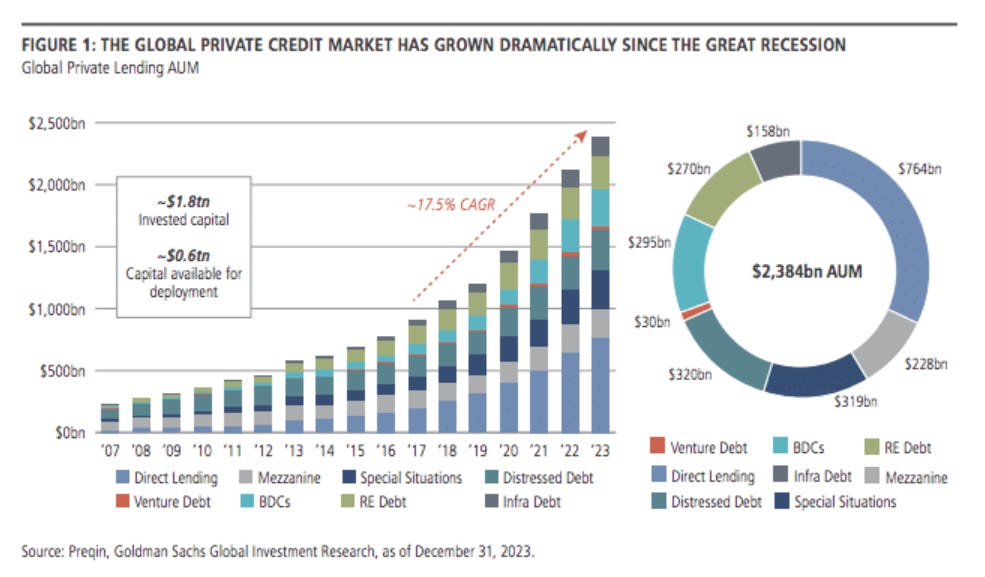

The explosive growth of private credit can be traced back to increased regulation on banks following the Global Financial Crisis. Capital requirements under frameworks like Basel III were designed to de-risk financial institutions by imposing stricter limits on their lending activities and requiring higher reserves. While effective in reducing systemic risk, these regulations inadvertently hampered banks' ability to take on certain types of loans, especially those perceived as riskier or more capital-intensive.

As a result, private credit funds, unencumbered by the same regulatory constraints, stepped in to fill the gap, growing from $200 billion in 2009 to over $2 trillion by the end of 2023. Today, they play a pivotal role in financing real estate projects, middle-market buyouts, and real estate loans. These sectors have benefited from private credit funds’ ability to lend where traditional banks have pulled back, and the providers of credit often enjoy very compelling risk-adjusted returns.

However, not all segments of lending have been equally disrupted—margin credit, in particular, remains a space where traditional financial institutions continue to thrive due to its inherent appeal: it’s collateralized, liquid, and historically low-risk.

While private credit has transformed many areas of lending, margin lending remains a stronghold for bank-owned brokerages. This is due to its unique balance sheet implications:

The crypto market presents an intriguing opportunity in the broader private credit narrative. Despite the rise of Bitcoin and other digital assets as significant financial instruments, traditional banks have largely avoided lending to related businesses or accepting crypto as collateral. The reasons are twofold:

This regulatory gap creates a unique opportunity for private credit providers to step in where banks cannot. Unlike traditional real estate or commercial loans, crypto-backed credit operates in a largely untapped market with attractive risk/return dynamics. Bitcoin, for example, has characteristics that make it comparable to blue-chip trillion-dollar market cap stocks like Nvidia:

Yet, because banks cannot underwrite loans collateralized by crypto, private lenders have the advantage of being first movers in this market. The demand for liquidity among digital asset holders—whether for margin credit or working capital—creates a compelling opportunity for those willing to navigate the space.

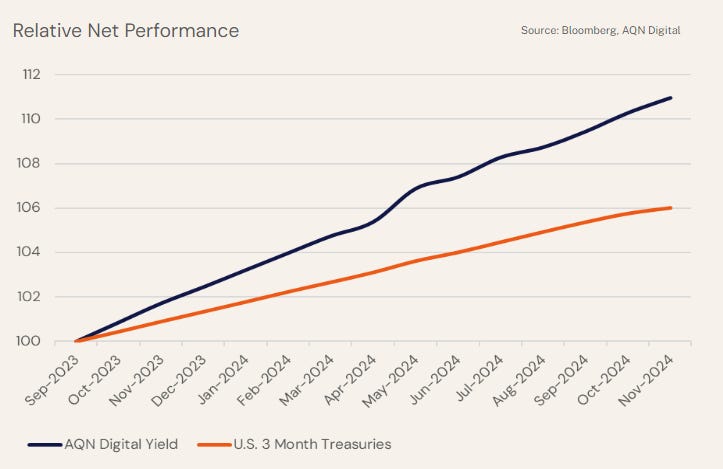

This is precisely where the AQN Digital yield fund operates. While it may be misinterpreted as a "crypto investment," the reality is that it functions as a private credit fund focused on a highly attractive segment of the market. By providing margin loans backed by crypto collateral, we offer:

The private credit boom underscores a broader trend: when traditional financial institutions step back, alternative players have the chance to step forward. Crypto is the next frontier in this evolution. With a market still underserved by traditional lenders, the opportunity to provide credit and liquidity to digital asset holders is unprecedented.

For investors seeking to capitalize on this shift, our income fund offers a unique entry point. By bridging the gap between crypto markets and private credit, we’re not just filling a void—we’re building the foundation for the next generation of financial innovation.

As private credit reshapes traditional lending, it’s time to look ahead—to new markets, new collateral, and new opportunities. The market is ready. Are you?

A: Private credit refers to non-bank lending, where private investors or funds provide loans to businesses and individuals. Its growth has been driven by stricter banking regulations, like Basel III, which have limited banks' ability to take on certain types of loans. As a result, private credit has expanded into areas like real estate financing, middle-market lending, and leveraged buyouts, offering compelling risk-adjusted returns.

A: Banks face significant regulatory and accounting challenges when dealing with crypto. Digital assets are classified as intangible assets, requiring write-downs in the event of price declines. Additionally, there is regulatory uncertainty and skepticism around crypto’s volatility and security. These hurdles make it impractical for banks to extend credit against crypto assets or hold them as collateral.

A: Crypto-backed loans are typically over-collateralized, reducing lender risk. Assets like Bitcoin are highly liquid, trade 24/7, and offer transparency through blockchain technology. These factors, combined with the growing demand for liquidity among crypto holders, create a unique and untapped market for private credit providers willing to navigate the space.

A: Bitcoin shares several characteristics with blue-chip stocks:

A: The AQN Digital Yield Fund focuses on providing margin loans backed by crypto collateral, positioning itself as a private credit fund, not a crypto investment fund. Key advantages include:

By addressing a gap left by traditional banks, the AQN Digital Yield Fund offers an attractive entry point into this high-growth private credit frontier.